credit scoring

Have you ever wondered why businesses sometimes struggle with cash flow despite making sales? The way sales transactions are recorded in accounting, particularly through debits and credits, may be one of the primary causes. A single sale has the potential to set off a series of financial events that, if recorded incorrectly, could result in financial mismanagement.

According to recent reports, 82% of small businesses fail due to poor financial management; understanding the role of debits and credits can help you avoid falling into this category. In accounting, debits and credits are the backbone of every transaction, yet they can be confusing, especially regarding sales.

Although sales transactions may appear simple, how they are recorded can significantly impact your company's financial health. In this article, we'll explore how debits and credits work from a sales perspective and help you master the art of recording sales transactions accurately.

Debits and credits are the two fundamental components that drive double-entry accounting. When one account is debited, another must be credited, ensuring that the accounting equation (Assets = Liabilities + Equity) always remains balanced. In terms of sales, debits and credits help track revenue, customer payments, and any adjustments like returns or discounts.

For instance, when a sale is made, the company receives either cash or a promise of cash (Accounts Receivable). In this transaction, the sales revenue account is credited, and the asset account (such as cash or accounts receivable) is debited. Businesses may maintain accurate financial statements and make informed decisions by knowing how these two factors interact.

Now that we have this basic understanding let's look into how debits and credits play a key role in sales transactions.

When it comes to sales transactions, the application of debits and credits can differ depending on the nature of the transaction. To make it clearer, let's divide this into two parts: sales credits and sales debits.

The above side-by-side comparison chart illustrates when to apply a debit versus a credit in sales transactions.

A debit entry in a sales transaction generally occurs when there is an increase in an asset or when an expense is recognized. When a business records a rise in its accounts receivable or cash accounts, representing the value of goods or services sold, it is the most typical situation for a debit in sales accounting. Here's how it works:

For example: If a customer buys products on credit for $500, the entry would look like this:

Pro Tip: Always debit the appropriate asset account depending on whether the sale is being paid for with cash or credit. This helps accurately track what is owed to the business or what has been received.

On the other hand, a credit entry happens when there is an increase in revenue, a liability, or the sales tax payable. When products or services are sold, the most common credit entry to sales revenue is made, representing the sale's value.

For Example: A customer buys products for $500, and the sale is subject to 10% sales tax. The journal entry would be:

In this case, you credit both Sales Revenue for the product sale and Sales Tax Payable for the sales tax collected.

Pro Tip: To guarantee compliance with tax laws, always credit the appropriate liability account when managing sales, including taxes.

After understanding the basics of sales debits and credits, knowing how these entries appear at various points within the sales cycle is essential. Let's examine how debits and credits change from the first order to the last payment and how each stage impacts your accounting.

The sales cycle is a series of steps a business follows, from the initial customer interaction to receiving payment. Debits and credits are crucial to maintaining correct financial records throughout this cycle. Here's a breakdown of how debits and credits work at each stage of the sales cycle:

The above flowchart shows the stages of the sales cycle and the associated debits and credits.

When a customer orders something but doesn't pay immediately, you record the amount the customer owes as an increase in Accounts Receivable and recognize the sale by crediting Sales Revenue.

Once the goods or services are delivered and the customer hasn't paid yet, the sale is still recorded the same way, crediting Sales Revenue and debiting Accounts Receivable.

When the customer makes payment, you debit Cash to reflect the increase in liquid assets, and you credit Accounts Receivable to show that the amount owed has been paid off.

You must reverse a portion of the initial transaction if the buyer returns the item or requests an allowance. You credit Accounts Receivable and debit Sales Returns and Allowances to reflect the adjustment.

After discussing how the sales cycle impacts debits and credits, let's examine how these transactions are formally recorded through journal entries to ensure that every sale is accurately reflected in your accounting system.

All debits and credits for every transaction are officially recorded in journal entries. Below are examples of how sales transactions would be entered into the journal for different scenarios using real business examples:

A clothing store sold a jacket for $500 in cash. The journal entry would look like this:

In this case, cash is debited because the store has received cash from the customer, and Sales Revenue is credited because the store has earned revenue from the sale.

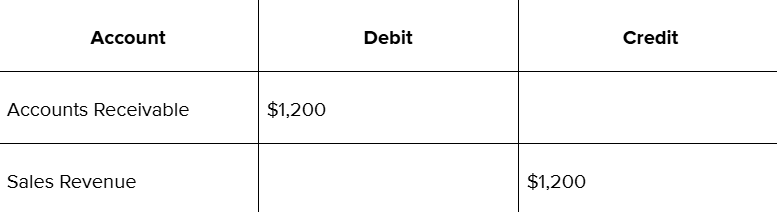

An electronics company sold a laptop worth $1,200 to a customer on credit, with payment due in 30 days. The journal entry would be:

Here, Accounts Receivable is debited because the business is owed money, and Sales Revenue is credited to reflect the sale of the laptop.

A restaurant sold a meal for $100, and the sales tax rate is 10%. The total amount charged to the customer is $110. The journal entry would be:

In this case, Accounts Receivable is debited for the total amount of $110 (meal + tax), Sales Revenue is credited for $100 (the sale), and Sales Tax Payable is credited for $10 (the tax collected).

A customer returns the jacket purchased earlier from a clothing store, valued at $500. The journal entry would reverse part of the original sale:

Here, Sales Returns and Allowances are debited to reflect the reduction in sales, and Accounts Receivable is credited to show that the customer no longer owes the business the $500.

An electronics company receives a payment of $1,200 from the customer who bought the laptop on credit 30 days ago. The journal entry would be:

In this case, cash is debited because the payment has been received, and accounts receivable is credited because the amount owed by the customer has been settled.

These examples illustrate how sales transactions are recorded at each stage, from the initial sale to payments and returns.

While debits and credits might seem straightforward, mistakes are common in sales accounting. The following are some of the most common mistakes businesses need to be aware of:

After identifying typical errors to avoid, let's examine some best practices for handling sales debits and credits to guarantee accuracy and effectiveness in your accounting processes.

Keeping correct financial records requires efficient debit and credit management. By adhering to best practices, businesses may guarantee consistency and lower the chance of mistakes. Below are some simple strategies to help streamline your sales accounting process:

South East Client Services (SECS) helps businesses streamline their accounting systems, integrating automated solutions to improve efficiency and reduce errors in managing debits and credits.

By following these best practices, you can ensure that your sales transactions are accurately documented and that your financial reporting is consistent, which will keep your company financially stable.

Understanding the role of debits and credits in sales accounting is essential for maintaining accurate financial records and avoiding costly errors. The proper accounting practices ensure your financial accounts stay accurate and current, from accurately documenting sales transactions to handling returns and taxes.

South East Client Services (SECS) helps businesses streamline their accounting systems, offering automated solutions that make managing debits and credits simple and efficient. Your sales accounting process can function more efficiently with SECS's experience, lowering manual errors and increasing overall accuracy.

Are you ready to streamline accounting practices? Get in touch with SECS right now to find out how our customized solutions can improve your financial management and keep your business on track!